.jpg)

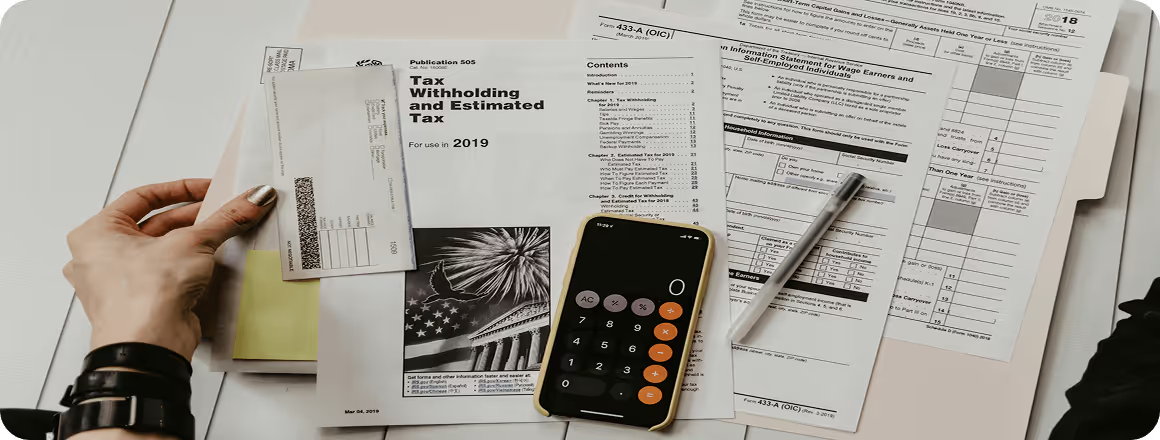

Tax audits are always a worrying moment for business owners. During documentary or factual inspections, controllers carefully examine all documents and working conditions of a sole proprietor or LLC. Even minor mistakes can become a reason for fines or other sanctions.

It is impossible to completely avoid an audit — the legislation of Ukraine provides that the STS may at any moment check whether the business is conducted in accordance with the rules and requirements of the Tax Code.

To avoid trouble, the main thing is to prepare in advance. It is important to understand what types of audits exist, how they are conducted, what controllers pay attention to, and which documents must be in order.

We will explain how to prepare a business in order to minimize risks and how an owner can protect their rights during an audit. This allows you to work calmly, without worrying about fines or unnecessary problems.

A tax audit is a way to ensure that a business conducts its activities honestly and pays taxes. Audits can be scheduled or unscheduled, documentary or factual — depending on the purpose and circumstances.

The STS may at any moment check a taxpayer: review declarations, the amount of taxes paid, request primary documents or the income record book. Inspectors may also visit the establishment or office directly to assess the correctness of employee registration, the use of RRO/PRRO, and compliance with other legal requirements.

Tax audits of sole proprietors and LLCs may be of different types — everything depends on the purpose of the inspection and the grounds provided by law (Art. 75 of the Tax Code of Ukraine).

They are conducted without prior notice directly at the place of business — in the office, shop, café, etc. The purpose of such audits is to assess the correctness of settlements, cash operations management, and compliance with labor legislation. And most importantly, it takes place without the presence of the owner.

They take place at the premises of the tax service, without the direct participation of the entrepreneur. During such audits, submitted declarations and paid taxes are analyzed in order to identify discrepancies or calculation errors. All available data on the activity are analyzed.

They may be scheduled or unscheduled, on-site or off-site. They involve the participation of the entrepreneur: the STS may require the provision of documents or the fulfillment of other requirements defined by law (Art. 20 of the Tax Code of Ukraine). It is precisely for this type of audit that the tax authority must send a notice 10 days in advance.

The procedure of the audit depends on its type. If we are talking about a factual on-site audit, it usually proceeds as follows:

Inspectors (necessarily consisting of two persons) conduct a control operation — purchase goods or order a dish at the establishment, without introducing themselves.

Then they present to the entrepreneur the audit direction, a copy of the order, and their official IDs.

The inspection lasts several hours; however, the term may be extended if there are legal grounds for this.

Based on the results of the audit, a report is drawn up in two copies, where identified violations are recorded, or a certificate of absence of problems if no violations are found.

Desk audits take place without the direct participation of the entrepreneur. After the completion of the inspection, the sole proprietor or LLC receives a report indicating the identified violations, and subsequently — a tax notification decision with the amounts of additionally assessed taxes or fines. If the entrepreneur disagrees with the conclusions, they have the right to submit objections to the report.

Documentary audits. Scheduled ones are conducted according to the approved schedule, unscheduled ones — by decision of the STS when information about possible violations is received. After completion of the audit, a report is also drawn up, which may be appealed in case of disagreement with its results. The tax authority must notify about such an audit — no later than 10 calendar days before its start. If we are talking about factual and desk audits, in such a case the tax authority is not obliged to notify about them.

There is time to prepare for scheduled audits, whereas factual audits may be unexpected. Therefore, sole proprietors and LLCs must always be ready: documents, cash registers (RRO/PRRO), licenses, and employment contracts must be in order.

To minimize risks, it is worth conducting business in accordance with legislation and engaging specialists who monitor changes in tax and other regulatory acts, properly prepare documents and accounting. It is also necessary to periodically check accounting, HR documents, and other aspects of activity, correcting errors and bringing everything into compliance with requirements.

Every month, all primary documents should be checked and reconciled with bank statements. It is important that payment purposes correspond to the registered types of activity, and that invoices, acts, or waybills are available for all income and expenses. If errors are detected, it is advisable, where possible, to correct everything or prepare clarification letters (an accounting certificate).

It is also necessary to ensure that documents are properly executed and contain all required details. In addition, the activity must correspond to the registered KVED codes, since violation of these requirements may lead to the loss of the simplified regime and additional tax assessments.

Every month it is worth checking the electronic cabinet of the STS: make sure that the accounting data, group, and taxation system are indicated correctly, and that submitted reports correspond to the primary documents. If errors are found, it is better to submit уточнюючі declarations independently — in such a case the fines are smaller than if they are detected during an audit.

It is also necessary to check for the presence of tax debt in the section “Status of settlements with the budget.” If there is a debt, it must be repaid. To make sure that there is no debt, it is recommended to order a certificate of absence of indebtedness through the electronic cabinet.

Before an audit, it is worth making sure that labor relations with all employees are formalized (all notifications of hiring have been submitted), and that HR documents (in an LLC — also military registration documents) are put in order. The tax authority checks compliance with labor legislation, and violations may lead to significant fines — for an unregistered employee the fine may exceed UAH 80,000.

It is also important to instruct staff on how to behave during an audit and appoint a responsible person to communicate with inspectors.

During a factual audit, it is important to properly build communication with STS inspectors: not to obstruct the audit, but to act strictly within the law. During documentary audits, a sole proprietor or LLC is obliged to provide the requested data in a timely manner. At the same time, it is important for the entrepreneur not only to comply with the requirements of the Tax Code, but also to clearly understand their rights.

The further steps of the entrepreneur are determined by the content of the audit report. Such a report is drawn up based on the results of any tax inspection. During a factual audit, it is prepared directly on-site in two copies or submitted for signature to the business owner or an authorized person at the premises of the tax authority after the completion of the audit. Based on the results of desk, documentary, or other audits, the report is sent to the entrepreneur after the completion of the inspection.

By contacting our experts, you receive comprehensive assistance at all stages of the audit:

Our specialists are well versed in all types of audits — factual, desk, documentary, scheduled, and unscheduled — and know what information the audit report must contain.

Submit an application to learn about the details of cooperation!

.avif)