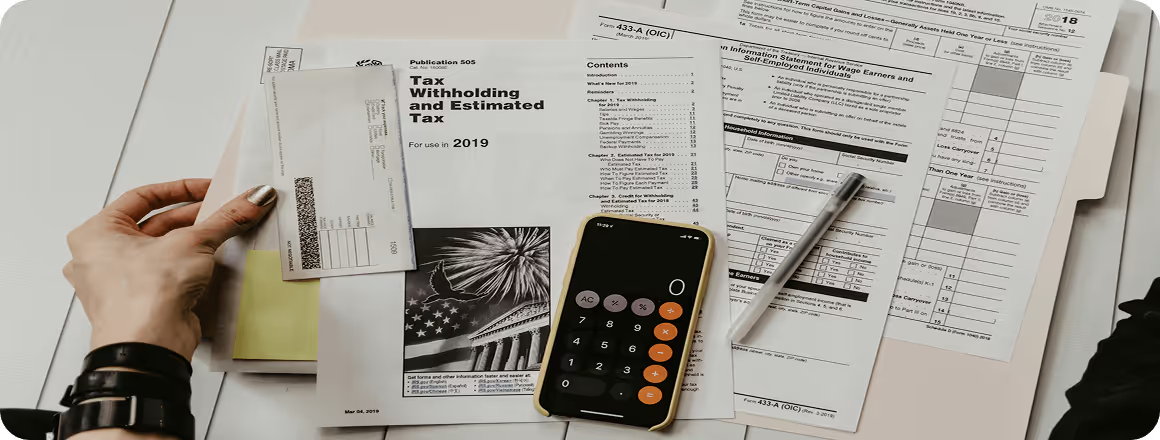

Ukrainian entrepreneurs, especially at the start, often have to deal not only with developing the business itself, but also with legal, tax, and accounting matters. And understanding the basics in areas related to business activity will never be unnecessary, at least from the point of view of checking the work of contractors or the team.

That is why we have prepared a short practical guide to source documents for LLCs: what they are, why they are needed, and why they should not be treated as a mere formality.

Source documents are documents in paper or electronic form that contain information about a company’s business transactions. In simple terms, they show what exactly happened in the business: when, between whom, for what amount, and on what basis.

For example, a company received a service, sold goods, paid an invoice, issued cash from the cash desk, or transferred goods to a buyer — all of this must be supported by a document. In legal terms, according to Article 9 of Law No. 996, “source documents are the basis for accounting records of business transactions.”

Legislation does not contain one exhaustive list of source documents for an LLC. These may include delivery notes, goods transport waybills, certificates of completed works or services rendered, cash receipt and cash expenditure orders, accounting notes, or other documents containing information about a business transaction.

Source documents are not just “papers for the accountant”; they are the basis of accounting and tax records. Without them, there are no grounds to record a transaction in accounting and reporting.

If, during an audit, the tax authorities see transactions that are not supported by “source documents,” the company will face questions. It will have to explain whether the transaction actually took place, why it was recorded without proper documents, and whether this affected tax indicators. The consequences may vary: from additional explanations to audits and fines.

But there is an important nuance: source documents do not automatically and unconditionally confirm the reality of a transaction. Even if all source documents are available, the tax authorities, “if there are reasonable doubts,” may request additional confirmation that the transaction actually took place. This may include a contract, a bank statement confirming payment, documents confirming the movement of goods, correspondence with the counterparty, etc.

A source document may be either paper-based or electronic. However, in any case, it must contain mandatory details, including:

the name of the document;

the date of preparation;

the name of the company on behalf of which the document was prepared;

the content and volume of the business transaction;

the unit of measurement of the transaction;

the positions of the persons responsible for carrying out the transaction and ensuring its proper documentation;

the signature of the person, including an electronic signature, who participated in the transaction.

Source documents, accounting registers, financial statements, and other reports must be prepared in Ukrainian.

If a document that serves as the basis for entries in accounting records is prepared in a foreign language, it must have an ordered authentic translation into Ukrainian.

From April 1, 2026, businesses may use a simplified approach to preparing certain source documents. The relevant changes were introduced by Law No. 4791-IX to Article 9 of the Law of Ukraine “On Accounting and Financial Reporting in Ukraine.”

What has changed: in certain cases, the absence of details on the part of the customer of services or works, or the lessee/tenant, is not considered a violation of the requirements for preparing a source document. However, important conditions must be met simultaneously: such a documentation procedure must be directly provided for in a written agreement, and business transactions must be reflected in accounting records in the period in which they are carried out.

In simple terms, in certain situations, an act or another source document may be prepared without the customer’s signature. But this does not mean that “acts are no longer needed” for all transactions or that document flow can be completely ignored. To use this simplification, the procedure for preparing documents must be provided for in the agreement in advance.

The simplification also does not apply to all business transactions. In particular, it does not apply to transactions paid for with public funds, lease agreements for state or municipal property, construction contracts and design and survey work contracts, as well as donation, charitable aid, or humanitarian aid agreements.

For a business owner, source documents are important not only during a tax audit. They are needed every day because quality accounting starts with them.

Timely and proper preparation of source documents helps to:

see the real income and expenses of the business;

obtain accurate data for management reporting, which we cover in a separate article;

control settlements with clients and suppliers;

minimize tax risks;

avoid mistakes in declaring tax liabilities;

have arguments in disputes with counterparties;

make management decisions based on facts rather than rough estimates.

Therefore, source documents are not a bureaucratic formality but part of the financial security of a business. The better a company organizes its document flow, the fewer risks it has in taxation, accounting, management, and relations with partners.

And the specialists of Alfa Gold are always ready to help organize high-quality work with source documents in your LLC.

.avif)