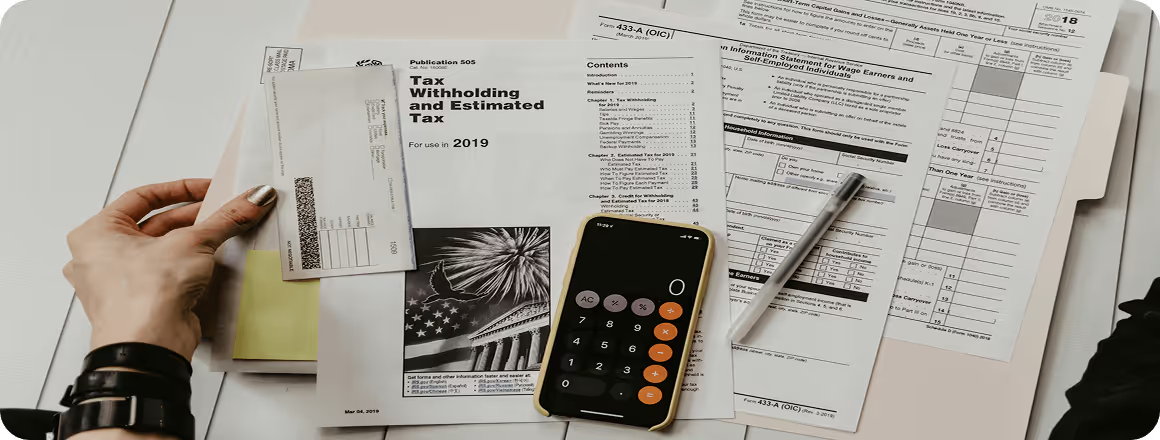

For many entrepreneurs, the value of management accounting is not obvious. It is often seen as the “younger brother” of financial accounting — something useful, but “not for everyone.” Partly because management accounting is not mandatory, and the state does not impose penalties for its absence.

However, it is management accounting that shows the business owner where the company actually earns money and where it loses it, which areas are worth developing, and which need to be reconsidered. For the transport business, this is especially important, because profit here depends on many components: fuel costs, empty mileage, downtime, route specifics, and other factors that are not covered by financial accounting, but can be identified through management accounting.

The main purpose of management accounting is to give the owner a complete and clear picture of the company’s financial condition. Based on this information, it becomes possible to see what works well in the business model, what needs improvement, and what, perhaps, should be abandoned.

How does this work in practice? Imagine that a transport company has two active routes on which it performs deliveries. The financial report shows that together they bring the company UAH 100,000 in profit per month. At first glance, everything looks good — the business is profitable.

But if financial accounting is supplemented with even a basic management report, the picture turns out to be different:

Route A has a profitability of UAH 150,000;

Route B generates a loss of UAH 50,000.

The first insight: the company earns money not because both routes are effective, but because one “pulls” the business forward, while the other takes away part of the profit. Even the simplest conclusion — to close the loss-making route — would immediately improve the financial result. But a high-quality management reporting system will show the reasons why the problematic route generates losses.

For example, reports may show that Route B has fuel consumption 30% higher than planned. The reason is that it passes through a large city during rush hour. Or that three drivers work on Route B, although the actual workload does not require this, while the profitable route, on the contrary, lacks drivers.

Another option is that Route A uses more expensive vehicles, but with lower base fuel consumption. The difference in cost will pay off after 100,000 kilometers of mileage, and after that savings begin. If the transport is used for many years, this is no longer just about fuel, but about a noticeable reduction in the cost of transportation.

Based on this information, the owner can make decisions that are not intuitive, but logical and based on real figures: change the route schedule, revise the tariff, find cargo for the return trip, redistribute drivers, increase the number of trips on the profitable route, or plan fleet modernization.

These are simplified examples, but the point is clear: a properly prepared management report helps calculate the expected effect of management decisions and shows ways to achieve the desired business indicators.

Despite the usefulness of this tool, management accounting is not common in transport companies. Many owners see only the overall financial result of the company, but do not see which routes, costs, and decisions it consists of. And that is exactly the point.

Before starting management accounting, it is necessary to determine what exactly should be analyzed in your business. In a transport company, such objects may include vehicles, routes, trips, drivers, clients, contracts, types of services, or separate transportation areas.

For example, analyzing fleet efficiency helps understand which vehicles actually generate money, and which are constantly being repaired, standing idle, or operating with low margins.

With clients, things are not always obvious either. A customer may provide a large volume of orders, but because of a low tariff, payment delays, complex logistics, or additional costs, they may be less profitable than a client with a smaller average check but simpler working conditions.

In short, management accounting in a transport company begins with the question: in which dimensions does the owner need to see profit, expenses, and business efficiency?

In a transport company, expenses are usually divided into variable and fixed costs.

Variable costs are those directly related to a specific trip: fuel, driver payment per trip, toll roads, customs duties, parking, loading or unloading costs.

Fixed costs are those the company has regardless of the number of completed trips: office, staff, communication, rent, and part of administrative expenses.

This division is needed so that the owner can see the real economics of transportation. A trip may look profitable if only revenue and fuel are counted. But if driver payment, toll roads, downtime, empty mileage, and other related expenses are added, it may turn out that the margin is minimal or nonexistent.

For operational management of a transport business, it is convenient to calculate trip profitability through variable costs. This way, the owner quickly sees how much the company earns on a specific order before covering fixed costs.

At the monthly level, it is necessary to analyze whether this margin is enough to cover all fixed costs of the company and generate net profit. Cash flow should also be monitored separately, because profitability and the availability of money in the account are not the same thing. A company may have profitable trips but still face cash gaps due to payment delays, large advance expenses for fuel, repairs, leasing, or taxes.

When it is clear what needs to be analyzed and how expenses should be calculated, the next step is to define what exactly should be considered a “good result.” For this, KPIs — key performance indicators — are used.

In a transport company, such indicators may include cost and revenue per 1 km of mileage, margin per trip, profitability of a route or vehicle, empty mileage ratio, fuel consumption per 100 km, fleet utilization, number of downtimes, repair costs for each vehicle, deviations of actual indicators from planned ones, and so on.

But it is important not to turn management accounting into dozens of tables that no one reads. Excessively detailed analytics can also become a problem: the owner and the team may simply get “buried” in data. KPIs should not exist “for show”; they should include only those indicators that are needed for decision-making.

With reports, it is possible to fall into the same trap as with KPIs: not all of them are needed by the owner, and an excessive number of reports can only blur the picture. Therefore, it is better to start with several basic management reports.

The Profit and Loss Statement, or P&L, shows whether the company is profitable, what income it receives, and what expenses it incurs. In the transport business, it is advisable to prepare such a report not only for the company as a whole, but also by routes, vehicles, clients, or transportation areas.

The Cash Flow Statement shows how much money actually came into the accounts, how much was spent, and whether there will be enough funds for fuel, salaries, repairs, and other payments. For transport companies, this is especially important because large current expenses often arise before clients pay for the services.

The Balance Sheet helps see the overall financial condition of the company: assets, liabilities, equity, debts, vehicles, loans, or leasing.

In addition to basic reports, a transport company should also have specialized ones. For example, a fleet report showing mileage, fuel costs, repairs, downtime, and profitability for each vehicle.

Some information is needed by the owner daily or weekly — cash movement, completed trips, fuel expenses, accounts receivable. These are data for operational management.

Other reports are enough to analyze once a month: route profitability, financial result, fleet efficiency, plan/fact analysis of expenses and income.

A clear reporting frequency and meeting deadlines help avoid creating unnecessary work for the team and prevent “data chaos,” where it is difficult to find truly important information.

Management accounting works fully only when it is properly automated. If all management accounting is maintained manually in Excel, over time it becomes inaccurate, untimely, and unsystematic. Spreadsheets may work at the start, but when the number of vehicles, trips, drivers, clients, and expenses grows, they quickly turn into a source of errors.

The optimal solution is to keep records in an ERP system that meets the needs of a transport company. Such systems can integrate with GPS monitoring, record actual mileage, help control fuel costs, pull data from fuel cards, work with waybills, trip accounting, settlements with counterparties, and management reporting.

This is important because management accounting must be not only accurate, but also operational. If the owner sees a problem a month after it occurred, the company has probably already lost money.

Management accounting is a very useful tool, but it will not work if financial accounting at the company is poorly maintained. Management reporting complements financial accounting, relies on it, but does not replace it.

For a management report to show real flows, problems, and weak points, it needs up-to-date data. If the primary figures are incorrect or incomplete, accurate analytics based on them is simply impossible. Therefore, the conclusion is simple: management reporting works only in combination with quality financial accounting.

Management accounting in a transport company is not just an analysis tool. It is a way to see the business in detail: by routes, vehicles, trips, clients, drivers, expenses, and money.

It is not a “magic pill” that will automatically increase revenue several times over. But one of the main problems of many businesses is that the owner does not see where the company actually earns money and where it loses it, and therefore cannot even basically optimize processes.

Often, after the first management reports, the owner starts looking at certain business areas differently. What seemed to be the “locomotive” of the business may turn out to be less profitable once all expenses are taken into account. And vice versa: a route or service that seemed secondary may begin to generate stable profit after small changes.

A management report itself is not magic, but it gives the owner the ability to make decisions based not on feelings, but on figures. And if management and financial accounting are built correctly, the company receives not just reports, but a predictable system for managing profitability. And Alfa Gold is always ready to help you with this.

.avif)